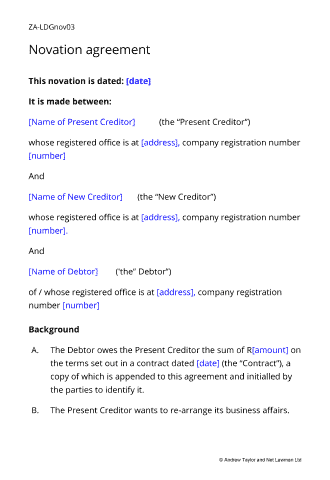

Novation agreement

Document overview

- Length:5 pages (1560 words)

- Available in:

Microsoft Word DOCX

Microsoft Word DOCX Apple Pages

Apple Pages RTF

RTF

If the document isn’t right for your circumstances for any reason, just tell us and we’ll refund you in full immediately.

We avoid legal terminology unless necessary. Plain English makes our documents easy to understand, easy to edit and more likely to be accepted.

You don’t need legal knowledge to use our documents. We explain what to edit and how in the guidance notes included at the end of the document.

Email us with questions about editing your document. Use our Lawyer Assist service if you’d like our legal team to check your document will do as you intend.

Our documents comply with the latest relevant law. Our lawyers regularly review how new law affects each document in our library.

About this novation agreement

Use this novation agreement to transfer the right to receive a debt repayment from one creditor to another (i.e. change who will receive the debt repayments). Common uses are when a business is sold and the purchaser takes on the assets of the seller, or when buying the debts of another party.

This is a simple yet comprehensive agreement that can be used to novate any right to receive a debt, usually with only minimal editing.

The basic law is that A cannot transfer to C the obligations he has under a contract with B, without B agreeing. So what happens is that all three enter into a “novation” agreement whereby the proposed transfer is made with B’s permission. Usually, B will want payment or some concession for his agreement.

The consent of all three parties - the transferee, the transferor and the other contracting party - is required to effect any novation. Unless you specifically require the consent of the other contracting party (perhaps because your contract has a non-assignment clause), our assignment agreement may be an even simpler way of transferring your contract to someone else.

Why not a deed of novation?

The deed format is used where one party to a contract receives no consideration. However, a novation is invariably "for value", and as such, a deed of novation confers little additional advantage.

In the unlikely event that a party agrees to novation out of pure kindness, the consideration can be entered as “one pound”, or a "peppercorn". The sum does not need to have any relation to the value of the debt being novated.

When to use this novation agreement

A common misconception is that novating a debt cancels an old debt and creates a new one to the new owner. Instead, novation just changes the parties to the original contract.

In most cases, novation is an easier option than cancelling and drawing new agreements.

This document can be used to transfer any debt between a creditor and a new party provided that the debtor agrees to the transfer.

Changing who will repay the debt

If you want to transfer the debt to another debtor (i.e. change who will repay the debt), then use of the Novation agreement: transfer debt to new debtor agreement will be more suitable.

Agreement features and contents

- Suitable when either party is resident outside the South Africa;

- Ensures a legal transfer as it is drawn as an agreement between all parties;

- Comprehensive provisions provide ideas for you to mould

The agreement contains the following sections:

- Details of the parties;

- Indemnity to protect both parties from loss, damage or legal liability once the debt is transferred;

- The novation;

- Existing claims: sets out how outstanding claims will be dealt with;

- Costs: identifies who will bear costs incurred to date;

- Other usual legal provisions in plain English.

Recent reviews

Choose the level of support you need

Document Only

This document

This document - Detailed guidance notes explaining how to edit each paragraph

Lawyer Assist

- This document

- Detailed guidance notes explaining how to edit each paragraph

- Unlimited email support - ask our legal team any question related to completing the document

- Review of your edited document by our legal team including:

- reporting on whether your changes comply with the law

- answering your questions about how to word a new clause or achieve an outcome

- checking that your use of defined terms is correct and consistent

- correcting spelling mistakes

- reformatting the document ready to sign

All rights reserved